Actually, the fact that Bitcoin can't inflate is the biggest tell it will never work as a currency. There are a set number of bitcoins that can be mined and no more after that. It's fundamentally incapable of inflating. And that's f**ing dumb for a currency. Inflation at certain levels is good and necessary. A deflationary currency makes certain low margin economic activity extremely unattractive versus just sticking your money under the mattress ('hodl' in other words). Inflation encourages spending, your money is worth more now then it is later, so if you're going to build that new building or design that new product, better to do it now. You want inflation low enough that it doesn't punish people for saving but still provides an incentive to spend now. Economists put that number at around 2 percent. Perfectly possible to save for a house or retirement but still enough to give a push. Deflationary currencies punish economic activity- if you have to take out a loan to accomplish something every day that goes by afterward the money you owe represents more and more real value without the numbers changing, representing a significant deterrent. Some of the worst economic crises in history, including the great depression, were marked by significant deflation.

I'm no bitcoin defender, but that's not really how inflation works. Inflation is not just an increase in the base money supply. For example, a supply chain crisis can cause inflation without the money supply changing at all. And central banks can control inflation by controlling lending without printing or destroying money. Lending creates "virtual money" that contributes to inflation, so one of the ways central banks control inflation is by increasing or decreasing interest rates.

Bitcoin makes these things much more difficult, of course, and would never be a good currency compared to what we have now. But the gold standard has almost exactly the same properties as bitcoin, and gold-backed currency worked okay in the US for a long time.

The gold-backed currency did not, in fact, work okay in the US for a long time. Between 1836 and the Great Depression, the economy went 3 or more years between recessions only 4 times. By comparison, the last three gaps between recessions were 7, 10, and 6 years; and it's now been 13 years since the last one.

Come on. The 1800s „recessions“ were minuscule at worst compared to today‘s global meltdowns happening every decade. Think about the Asian crisis of the 1990s, the New Economy bubble burst at the beginning of the 2000s, the sub prime crisis 12 years ago and now a post Covid recession.

Also you‘re taking one feature „they had a gold standard back then“ and take it as the single point failure. In reality having a „Gold Standard“ does not guarantee a non-inflating currency. In the 1920s the FED was printing more dollars than were backed by gold to pay back the government’s war time debts. The same happened in the losing nations like e.g. Germany, too, in a much greater force causing a death spiral completely destroying the German Reichsmark. In the US you were lucky to just experience a stock market boom that spectacularly burst in 1929. This would have caused a recession for sure. However, the decade long depression that actually followed was a result of unprecedented economic meddling by the federal government under Hoover and then Roosevelt.

The Gold Standard was removed after the „Bretton-Woods“ system broke down in 1971. That was an attempt at establishing an international currency system with fixed exchange rates. It worked in a pyramidal fashion: The US promised to have their Dollars backed by gold and the middle power nations‘ central banks backed their currencies with US dollars. Of course, the US printed more dollars than they actually could back by their gold reserves. At some point France demanded to redeem their dollar reserves in Gold. The US did not comply and in 1971 Nixon declared the Dollar not being redeemable into Gold any more because the FED didn’t have enough gold left. Since then the US dollar as well as all international currencies are backed only by the people’s trust in them and by the fact you have to pay your taxes in those currencies.

So you see the monetary history is primarily a history of failure induced by bad economic policies. How currencies were implemented is just of secondary interest.

Bitcoin could easily serve as an international currency compared to the US dollar. Its value is based on trust like the US dollar. Governments could collect their taxes in the form of bitcoin if their wanted to without a major systemic change. And unlike the Dollar or Euro, Bitcoin couldn’t be inflated. Whether that will happen and change economy for the better is still left to be seen.

>Come on. The 1800s „recessions“ were minuscule at worst compared to today‘s global meltdowns happening every decade. Think about the Asian crisis of the 1990s, the New Economy bubble burst at the beginning of the 2000s, the sub prime crisis 12 years ago and now a post Covid recession.

This is completely wrong. The crash of 1873 began what historians call a 20-year depression. The Panic of 1893 was so serious that when Grover Cleveland needed oral surgery for cancer it was done in secret to avoid further panicking the country. J. P. Morgan basically bailed out the entire US economy in the Panic of 1907.

In all of these cases, labor unrest from the unemployed far exceeded anything seen in any post-WW2 economic crisis in the US. At multiple times the US treasury faced the prospect of being unable to fully redeem demands for gold in exchange for paper money. For the entirety of the Gilded Age, the two main political issues in the US were protectionism and free silver, both fundamentally tied into how the US economy functioned and how the US government paid for itself.

> J. P. Morgan basically bailed out the entire US economy in the Panic of 1907.

That says more about the size of the US economy at that time than about the size of the economic crisis…

Are you honestly comparing the Asian crisis with what happened in the US 120 years ago?

> This is completely wrong. The crash of 1873 began what historians call a 20-year depression.

Well, just a couple of years earlier the US was in the middle of a bloody civil war that was financed with monetary inflation. That is to blame the post war depression. Not the Gold Standard per se.

You are also conviently evading my main argument that the „Gold Standard“ is irrelevant to the discussion about Bitcoins inherent design. Bitcoin does not implement a Gold Standard even if it is called „digital gold“. It is a machinery designed to prevent human meddling with a monetary base. Something that the Gold Standard was better than today‘s fiat money. But of course it was still far from perfect and depended on the honesty of politicians and bankers.

So — forget about the Gold Standard. It will never come back. The promise of Bitcoin is to bring a monetary system politicians and bankers cannot manipulate. Whether that’s a good thing or even realistic is a separate discussion.

> The promise of Bitcoin is to bring a monetary system politicians and bankers cannot manipulate. Whether that’s a good thing or even realistic is a separate discussion.

Never heard of any politician giving up power voluntarely.

And money is the power: no more printing - need to work hard for money.

Actually not true. A lot of the 19th century recessions were "global" in that there was contagion across the Atlantic to Europe (or vice versa). Asia didn't get linked into the network until the end of the 19th century.

And the US money supply in the 1920´s was pretty stable as it happens, the 1929 bubble was a lending phenomena.

> The 1800s „recessions“ were minuscule at worst compared to today‘s global meltdowns happening every decade.

One of those recessions (the panic of 1857) was one of the main contributing factors to the American Civil War breaking out, which hardly seems ‘minuscule’.

Are you thinking that the South would have willingly given up slavery or that the North wouldn't have pushed the issue if this recession hadn't happened? Would we still have slavery in the South today, or would the war just happen some years later?

The North was willing to leave slavery in the hands of the States. Maybe without the pressure of a reccession the South would have accepted that compromise, and we had seen a quite different story of the USA until today.

Wasn't slavery already outlawed in the Northern states? I thought one of the main points of tension was the refusal of Northern states to recognize slaves that fled to the North as "property" and "return them to their owners".

> The North was willing to leave slavery in the hands of the States.

The South was unwilling to accept that the North didn't recognise slavery in its territory.

Southerners wanted slavery to be recognised and enforced throughout the US.

> I thought one of the main points of tension was the refusal of Northern states to recognize slaves that fled to the North as "property" and "return them to their owners".

That was the official line — and rather obviously against the concept of states' rights.

But for my money the main issue for the "gentlefolks" was that they couldn't bear not being waited on hand and foot by their slave retinues while enjoying the trapping of the north: they had to pick between those trappings and having an enslaved retinue, as any slave they brought up north was a jump and skip away from freedom.

And they really couldn't handle the "inconvenience" and "degradation".

I don't know that part of history, but I know it would be much more fun to read this discussion and learn from you guys if there wasn't a moving of goal posts. Also, I'd like to actually see your counter argument, and not just a statement that OP is wrong without anything else. Preferably against the point OP actually made.

> By the end of the Panic, in 1859, tensions between the North and South regarding the issue of slavery in the United States were increasing.

But it does not say that this was a direct result of the panic.

> The Panic of 1857 encouraged those in the South who believed the North needed the South to keep a stabilized economy, and southern threats of secession were temporarily quelled. Southerners believed that the Panic of 1857 made the North "more amenable to southern demands" and would help to keep slavery alive in the United States.

Sounds inconclusive to me, in the context of evaluating OPs argument. So I still don't know who is more or less right...

this kind of assumes that the only goal of an economy is to avoid recessions. growth is also very important to the average person, and the gold standard does not optimize for that

Optimizing for ever higher economic prosperity has so far had the side-effect of ever higher economic inequality, in no small part because only a small number of people are able to succesfully get rich off of moments of instablity.

Optimising for stability means less homless people on the streets (which is an appaling situation in US which still despite that wants to call itself a first world country) because a larger part of society can plan their futures and actually have those plans come true. This also necessary includes socialised healthcare and schooling, for the same reasons (which again probably won't happen in the US for the forseeable future).

That’s because the banks issued more gold certificates than they had reserves. Those bank shenanigans were the origin story of fractional reserve banking.

To clarify, the word "recession" has a strongly defined meaning. It does not mean "things are bad" although bad times are strongly associated with recessions. Things can seem bad even without a recession.

Historically speaking, each time we climb out of a recession over the last 50 years it's been a bit slower of a climb than the previous climb out. That is a worrisome trend in its own right. I believe that's the kind of bad you feel people are experiencing -- a barely perceptible improvement starting from a bad situation.

> Inflation is not just an increase in the base money supply.

Actually it can. During WWII, Germany was trying to make enough counterfeits and launder it to destabilize the allied powers' currencies. Many third world countries ended up remaining poor because their political leaders printed as much money as they wanted.

> But the gold standard has almost exactly the same properties as bitcoin, and gold-backed currency worked okay in the US for a long time.

God only filed some of the gold under the ground in the USA. He filed the rest of it elsewhere. The currency would then be based upon how much gold was mined and third parties could potentially be in control of the US currency.

As one freshwater economists argued: "Why gold? Why not french bordeaux?"

> And central banks can control inflation by controlling lending without printing or destroying money.

Lending is printing and destroying money. Central banks cannot control lending by changing interest rates as we have seen since the GFC. They couldn't get inflation up for ten years, and now they can't keep it down.

The belief in central banks and gold (why are gold miners so special?) is just as much of a cult as cryptocurrency.

All prices are relative, that's why they move all over the place.

> Lending is printing and destroying money. Central banks cannot control lending by changing interest rates as we have seen since the GFC. They couldn't get inflation up for ten years, and now they can't keep it down.

I beg to differ, asset prices experienced massive inflation during that period. Obviously, nobody was borrowing money to buy loads of hamburgers or other things that greatly influence the CPI. That demand is mostly inelastic and asset prices have little influence on it. That said, government spending accounts for almost half of spending in total. If this is increasingly financed by (the equivalent of) debt monetization, you will see debt chasing the hamburgers as well, causing runaway inflation like in Turkey. The central banks are very much in control of that not happening.

"I beg to differ, asset prices experienced massive inflation during that period."

Massive inflation, or just a return to their free market value.

Setting interest rates is an artificial market intervention. In a free market the base cost of money is zero, since it can be produced on demand at the push of a button.

The private price of money is then determined correctly by market action based upon credit risk and/or exchange risk.

Lending is often talked about as "printing money" but isn't investing in anything other than money also able to do the same thing?

Some seed investor puts a million pieces of money into a company, that company starts getting a lot of customers, new people are willing to pay much more for pieces of that company. But now this company has gone from zero to lots of value, and so that first investor can behave like they now have a billion pieces of money instead of the million they had originally (whether that's cashing out a small amount, or borrowing against it). So if the economy grows in a non-zero-sum way, how do you avoid inflation? The total value in the system (due to the circulation of money and the productive activity) goes up, and lots of it isn't in the form of "pieces of currency."

Is there so much difference between "lending money" - giving money on the belief that the counterparty will pay you back more over time - and "investing" - giving money on the belief that the share of the thing will be worth more over time? In the absence of regulations, even someone like a bank who's holding other people's deposits could do either sort of investment (and so is VC just a special sort of "bank")?

The way I think of it is that when you make a purchase, the money just basically switches bank accounts. The money is still in the banks, and currency is not created or destroyed, just exchanged between players.

When a bank makes a loan using it's customer's money, the balance in the account doesn't disappear -- and the money is still available to the customers. But now a loan for a car financed by a bank goes into the car dealer's bank account which then gets loaned out by that bank. This happens over and over again in a recursive manner. This is the Monetary Multiplier Effect as part of Fractional Reserve Banking.

It's basically kind of a regulated shell game. The bank has to have so much in cash to pay out in case of a bank run, and the FDIC protects customers from bad bank management. But your money is literally replaced with a number in an account balance. And your $10k in the bank might generate $40k of loans in the economy based upon your deposit.

An investment however removes cash from your account and replaces it with shares and that money is given to someone else. So it's an exchange of money and an exchange of shares. And thereby doesn't have the same multiplication effect. In this case value is created or lost which makes your shares worth more or less on the market.

Again, value doesn't create money. Money is exchanged between parties for different amounts. A 1981 bordeaux doesn't create currency over time, just increases it's value.

Fractional reserve banking directly inflates the economy via loans. If I deposit $1000 into my bank account, the bank will lend it to someone else instead of just holding it for me. That loan is new money created out of literally nowhere. It only becomes real money when the borrower actually extracts value from this world and earns real dollars in the process. The loan's repayment makes it real. Until that happens, the money doesn't actually exist, it's completely made up.

So borrower goes out and buys the stuff they need to make it happen. That money eventually ends up right back in the bank as a deposit. Once at the bank, it is once again loaned, spent, deposited, loaned, spent, deposited... Quickly inflating $1000 into a whole economic system worth huge figures like $100,000, not one cent of it real until all of the aforementioned economic activity actually succeeds in generating some real value. Always at risk of the whole stack unwinding due to business failures leading to defaults on loans which could cause even more defaults and liquidations and foreclosures and losses and all sorts of problems.

Multiplying that by an entire country's polulation results in truly mind-boggling amounts of money generation and therefore inflation. The actual money supply doesn't actually matter since it's a small fraction of the amount of money that's actually circulating.

The funniest part is cryptocurrency exchanges have turned into banks. They offer bitcoin lending services, savings accounts. Finite bitcoin supply? It doesn't matter. Value can always be inflated away through loans.

I’m not really following this. Let’s say I secretly tag my dollars with a red mark. Deposit $1000 cash, and then my account shows a $1000 balance. My red $1000 is probably going to wind up being withdrawn in an ATM by someone else, or used in a mortgage, or something else, but my red tagged $1000 bills don’t suddenly become a multiplied amount of money!

That is what the average person thinks what happens but in reality the bank does not even care about your deposit. What actually happens is that the bank just creates a new money from thin air by just adding another zero their account and then transferring some of that new money to the person who wants a loan.

The US fed does this too, they add a zero at the end of the existing account and create more money. Its all in a database no cash is being printed.

Then I go to the bank and request a $900 loan. It knows it has $1000 lying around doing nothing useful so it just gives a fraction of it to me as a loan. The bank does the following:

So the bank received a $1000 deposit, kept a $100 reserve and loaned out $900.

That $900 is completely made up money. They just credited my account with that amount out of nowhere. I'm supposed to go out there and earn money to pay it back. If I do, all is well. If I default? The bank has its books showing they owe you $1000 but they only have $100 in reserve. The illusion is shattered the second you attempt to withdraw that money.

In the real world, it's not just you and me. It's banks leveraging their massive reserves on risky loans and investments that fail, thousands of customers noticing and attempting to withdraw everything they have all at the same time, getting nothing, leading them to default on their debts and so on and so on until the government literally manufactures even more money to bail out the banks by "injecting liquidity" into them and restoring their reserves, putting an end to the bank run at the cost of even more inflation.

So I decide to spend that $900 on a computer for software development in order to work remotely. I go to the store and buy one.

The bank just received a $900 deposit, so its original reserves are restored. This means another loan is possible! This cycle repeats itself many times as money circulates until millions have been created out of thin air. Notice that the only way those accounts balance is if I pay back my $900 loan. If I lose my job before that happens? They won't balance and the bank will have to pick and choose who can withdraw and how much.

Not too long ago, Binance had restrictions on bitcoin withdrawals. Unverified accounts could only withdraw a small amount per day, verified accounts could withdraw a larger but still limited sum. Hmm...

I still don’t see the problem. At no point is cash conservation broken. They may say that my account has $900 in it when that cash doesn’t exist, it’s been used for some other end, but that’s not weird or unusual, or even interesting. I know that the bank has plenty of other peoples’ $900 that if I wanted that cash I could take it.

The problem is banks operate in a state of perpetual insolvency. Their ability to pay off their debts to customers depends on the state of the larger economy. Too many defaults and the whole thing comes crashing down.

> At no point is cash conservation broken.

It never existed to begin with. All that's required for the illusion to disappear is for enough people to attempt to withdraw funds at the same time.

> I know that the bank has plenty of other peoples’ $900 that if I wanted that cash I could take it.

> The International Monetary Fund estimated that large U.S. and European banks lost more than $1 trillion on toxic assets and from bad loans

> Lack of investor confidence in bank solvency and declines in credit availability led to plummeting stock and commodity prices

> The crisis rapidly spread into a global economic shock, resulting in several bank failures

> The de-leveraging of financial institutions, as assets were sold to pay back obligations that could not be refinanced in frozen credit markets, further accelerated the solvency crisis

> governments and central banks provided then-unprecedented trillions of dollars in bailouts and stimulus, including expansive fiscal policy and monetary policy to offset the decline in consumption and lending capacity, avoid a further collapse, encourage lending, restore faith in the integral commercial paper markets, avoid the risk of a deflationary spiral, and provide banks with enough funds to allow customers to make withdrawals

People complain about Tether but the whole banking system is just Tether on steroids.

> People complain about Tether but the whole banking system is just Tether on steroids.

With regulation, and audits, and insurance, and government guarantees that if something goes really wrong you will be made whole (as long as you don't deposit more than 7 years the median US income).

I also wouldn't deposit my money in an 1890's US bank.

You’re just repeating the same thing over and over. I still don’t think at any point the bank is multiplying money in any kind of real or concerning way.

You should really read up on this. He explains it fairly well, and yes, money are multiplied with fractional reserve banking. Since the bank only needs to keep a fraction of the money they owe to account holders, they can loan the rest out. But the point is that this loaned money ends up on some other customers bank account, possibly with the same bank, and can thus be loaned out again. So in a 20% reserve requirement situation, _the same money_ can be used to finance the building of five houses, not just one which it would be if the reserve requirement was 100%.

Banks duplicate your money endlessly. After money that existed only in your possession is deposited at a bank, it will exist in many places simultaneously: in your account, in other people's accounts, as loans to third parties. If you don't see how that inflates the money supply, then I'm not sure what else I can say.

This is what fuels exponential growth of nations. Banks keep conjuring up money out of thin air and loaning out to people so they can work and extract value out of this planet at unsustainable exponential rates. Humanity is addicted to it. The second these loans become unavailable for any reason, everything comes crashing down. The economy literally grinds to a halt.

Worst of all is these banks essentially dictate the direction future society will take. They choose who receives loans and who's left out in the cold. People like Larry Fink, CEO of BlackRock and manager of 10 trillion dollars. They decide things and then say "will you lead, or will you be led?"

Perhaps you're getting hung up over physical bank notes. If most people and companies hold most of their money as numbers in bank accounts and do most of their buying and selling by moving numbers between bank accounts, why is it only cash that matters?

The money is the numbers the banks report to you. Multiplying those numbers is inflating the money supply. Yes they might be required to hold some other assets than simply numbers in their databases to start the whole process, but they can still multiply money to some degree.

> It knows it has $1000 lying around doing nothing useful so it just gives a fraction of it to me as a loan. The bank does the following:

The bank does not have to do this everytime, Most of times it just creates a loan account and adds a number in the database and creates money out of thin air.

> Fractional-reserve banking is the system of banking operating in almost all countries worldwide

> under which banks that take deposits from the public are required to hold a proportion of their deposit liabilities in liquid assets as a reserve, and are at liberty to lend the remainder to borrowers

> Lending creates "virtual money" that contributes to inflation, so one of the ways central banks control inflation is by increasing or decreasing interest rates.

One way to understand how this works is by visualizing the circulation of the monetary base, aka physical coins and central bank reserves, or bitcoins/lunas in the crypto case.

Without lending, you have people and companies entering transactions, accumulating money and saving them for a later investment, for example putting a penny in the mattress or a bitcoin in cold storage. The penny might physically change hands once or twice a year. So in agregate you have:

V = PQ/M

with V, velocity of money ( = 1 transaction per year), PQ is the gross product (price level * quantity of goods), and M is the money supply (say, 21 milion bitcoins).

So one way to generate inflation is to increase M (print more money), since the ability of the economy to produce goods changes slowly, so P will need to increase to maintain equilibrium.

But another way to do that is to promote lending: instead of placing the penny in the mattress, is is deposited to a bank who immediately places it in the hands of a lender who buys a house or a TV, giving it to another entity that deposits into a bank etc. So you have a physical penny on steroids that can travel with a much higher velocity in the economic system, say 8 transactions per year as it was typical for the dollar last time I estimated this.

Banks can effectively print unlimited money substitutes (deposits denominated in bitcoins, luna, pennies etc) and as long as depositors trust them to be solvent this entire virtual monetary base will participate in the MV=PQ equation.

This is true in a fiat world as well as in a Bitcoin world, unregulated banks can greatly amplify the velocity of bitcoins without any technical support from the currency itself, in effect putting significantly more bitcoins on the market available for transactions, so overall reducing their market value, or "creating inflation" without printing a single bitcoin.

Indeed, the book Money by Jacob Goldstein, co-host of NPR podcast Planet Money, talks precisely about this in regards to the gold standard. One reason that it was taken off the gold standard was because monetary policy could not be fully leveraged well when every dollar was worth some amount of gold. One couldn't print new money during recessions to restart the economy, and one couldn't remove dollars from the money supply in a boom period.

Economic models, Keynesian or otherwise, are attacked and misapplied because individual players are better off with a larger slice of a smaller pie. Which doesn’t inherently invalidate these models, but few care about accuracy when billions of dollars are involved. When people talk about say ‘cap and trade’ what they really mean is give us a giant subsidy.

Is that a joke website or are they actually trying to tie the end of Breton woods to the quadrupling of lawyers per capita since 1971?

The number of people who drown in a pool strongly correlates with how many films Nicolas Cage has appeared in [0] but that doesn't make it a causation.

The era between 1945 and 1971 was not based on gold standard, but it was Bretton Woods system, that worked in a significantly different way from both era before (traditional gold standard) and era after (floating currencies).

Economic inequality has massively increased since abandoning the gold standard. Of course academic economists carry water for the people at the top benefitting from the inequality.

So has economic productivity, total activity, and overall quality of life.

So how do you decide which correlations to believe in more than other?

I believe economic inequality is a problem, but the gold standard would be throwing the baby out with the bathwater, based on weak "look, these things happened at the same time" reasoning.

Economic inequality has been MASSIVE at many times in the past prior to modern currency, after all.

Inequality has increased but poverty has decreased. The world is so much wealthier now.

Yes high inequality is a problem but I'd argue too low inequality is a problem too. You need a difference of outcomes to motivate people. If that doesn't happen in currency it will happen in another way. For example people will invest in political power and work hard to corrupt the system in their favor. This happens with high levels of inequality but is reduced as there is a legitimate path to improving ones lot. There is something competitive in us the drives us to do better than our neighbors. That needs a legitimate outlet.

> Inequality has increased but poverty has decreased. The world is so much wealthier now.

Perhaps, but this is largely a result of manufacturing (a primary source of middle class jobs) moving from developed nations to previously agrarian economies. The same cycles will repeat itself until there are no pockets of cheap labor left in the world for the owners of these corporations to exploit.

It seems plainly obvious that history shows the opposite is true; corruption is increased when money and power are centralized amongst a few people. There's a reason the term "Robber Baron" came around the last time we experienced massive inequality as a country. If you have some examples to the contrary I would love to hear them.

Has it though? If piracy is the act of invading someone’s private space where they can be isolated them from help and taking from them, is ransomware just modern piracy with less violence?

Of course the sea pirates are still very active on some areas.

This is meaningless without more detailed numbers. If it's held steady or gone up by a few percent while, say, the percent of wealth and income received by them has gone up far more, then... whoops. They're better off.

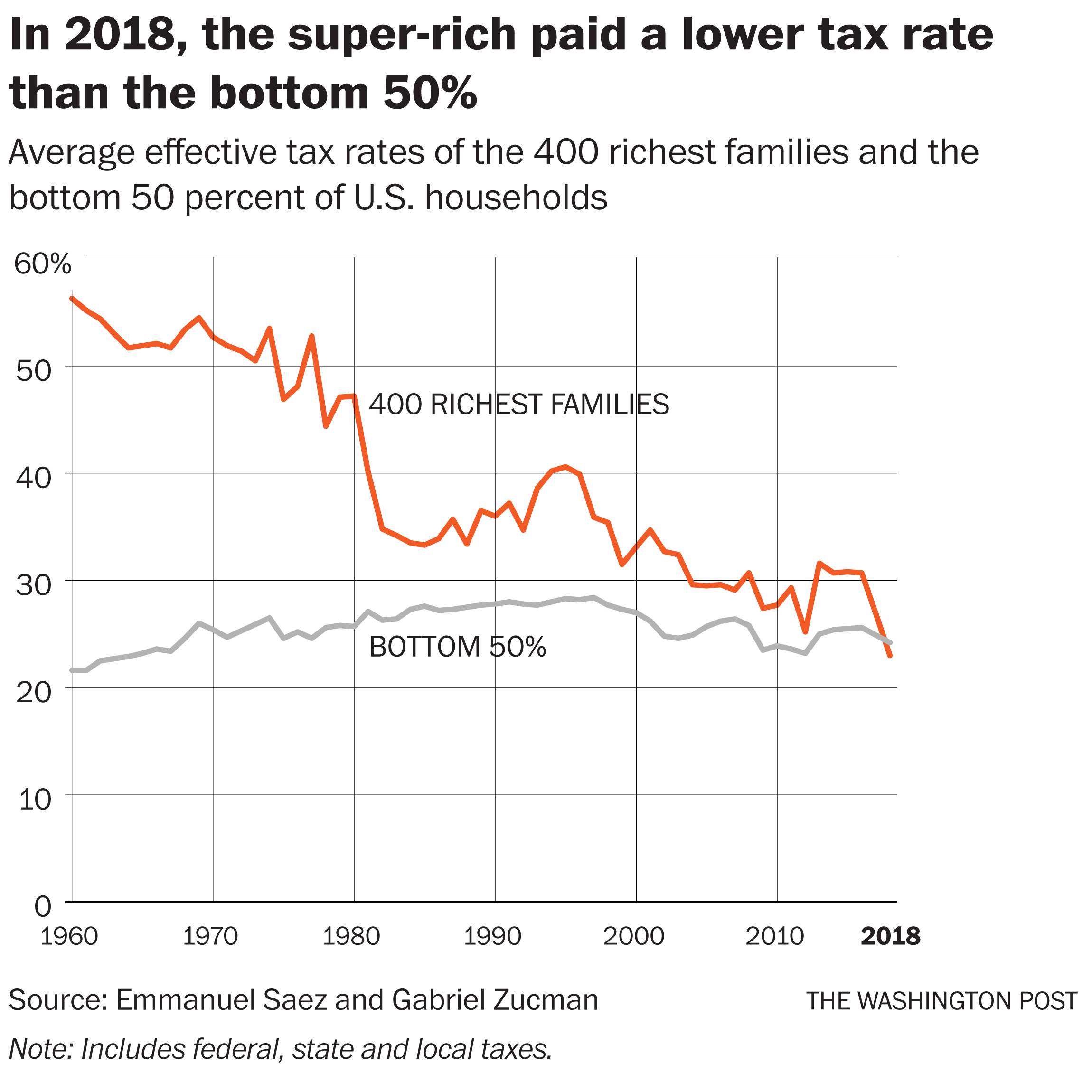

Well the percent of the GDP that is taxed is pretty steady at 20%, which infers that spending/taxes grows at the same rate as income. Thus the rich are paying the same percent or more of their annual income over time.

This does not follow at all from those numbers (and reality). Tax pressure has moved towards the middle and lower class, to ease the “burden” of the rich and wealthy.

Look, if the top 1% of people used to share 10% of a country's earnings, but now share 20% of a country's earnings, their relative contribution to total tax revenue will grow without any change to the tax regime.

So you need to consider the change in income distribution alongside any change in relative tax contributions. Otherwise the stats you cite are pretty meaningless

Looking at 2007 was a peak in both income earned and taxes paid. Comparing it to today, income earned (as a %) decreased, yet taxes paid (as a % of total) is about the same.

So we can at least say from 2007 to now, tax burden increased.

The tax burden for the top 1% _income_ earners can totally increase while the tax burden for the top 1% wealthy decreases (they earn from dividends, not work)

Keep in mind that not everyone pays taxes on capital gains. People with a lot of appreciated stock can simply borrow using the stock as collateral, and not pay a single penny in capital gains. Depending on the entity that owns the stock, the interest on the loan might even be deductible.

I hear a lot about that, but in reality it makes no sense. At some point in time the loan needs to be repaid and equity sold which carries a tax burden.

You could "step up" the basis when you die, but I find it hard to believe some billionaire would roll over debt for 30+ years, pay 200-300% in interest, just to avoid 20% long-term capital gains?

I read a lot of conjecture about how this happens and many people said Musk did this, yet he paid $500M in taxes last year?!?

> I find it hard to believe some billionaire would roll over debt

Plenty of rich individuals do exactly that, though. Hang out in any retirement/investing forum and you see people doing the cold hard math and deciding not to sell the stock and pay taxes if the step-up basis is enough.

You don't even need a significant return on capital for the strategy to pay off, it just has to slightly beat the interest on the loan over a very long time horizon. Consider these numbers: $100 million subject to capital gains, $10 million in cash needed for expenses, a 2% interest rate, a 2.5% return on investment, a 20% capital gains tax, and a 10 year timeframe.

The borrowing strategy starts with $100 million and a $10 million loan, and ends up with $128 million and a $12.2 million loan, so net $115.6 million (and the interest is likely tax deductible).

The taxpaying strategy starts with $88 million and ends up with $112.65 million.

> A deflationary currency makes certain low margin economic activity extremely unattractive versus just sticking your money under the mattress

We can't say that is a bad thing. A lot of that marginal economic activity is probably consuming resources that could have been better saved for a rainy day.

I'm all for economic activity, but the trying to incentivise people to consume everything they can is a bad outcome - someone doing something productive then putting money under a mattress is a fine outcome. If something unexpected comes up they'll have savings.

Putting money under the mattress is an awful outcome.

If people want to save then they should put their money in to a _bank account_ where they can earn interest and their money can be put to use productively.

Not only does this mean they’ll have savings, but it’s also safer (can’t get robbed) and it leads to the positive outcomes GP described around things actually getting built, and the saver ends up with more money than before because your bank account has a positive interest rate.

Where this fails is if the currency is deflationary, because then it’s extremely hard for the bank to offer a non-negative interest rate and so it really is more attractive to put money under the bed, modulo the risk of it being stolen or lost

Under the current system yes. People do need a savings technology. Not everyone should have to be a part time investor. Gold was that technology but it didn't survive the tech transition. Now we have Bitcoin trying to continue gold's mission.

If the currency was not inflationary, people saving would mean that everyone else's money becomes more valuable. You save first, then you invest. Not the other way around. Unless you want dumb money pilling in everything and creating mega bubbles that will burst and destroy everyone's value.

I guess you are not living in Europe (or Germany for that matter) where interest rates are now negative and you are actually paying 0.5% for the service of the bank holding your money.

Central bank interest rates are negative but consumer savings accounts are not negative. A quick google search shows that savings accounts are offering either zero or nominally positive rates (0.02%). I agree that interest rates are super low in Europe right now but they aren't actually negative for consumers.

In Germany, as an existing customer, you have negative rates with many banks.

You also don’t switch banks on a whim. Not only because it’s a hassle to change your payment info on dozens of sites, but also because you’re going to be punished by SCHUFA, a corporate abomination that has a monopoly on credit ratings. Their algorithms try to infer financial responsibility from

how many bank accounts you have (fewer is better), and from how often you open new bank accounts (rarely is better). Once it decides to punish you for shopping around, its effects are devastating.

Well then you will have to tell that to the banks. I am not claiming that because I read it somewhere but because of firsthand experience.

They are not calling it negative interest rate but "Verwahrungsgeld", so basically a fee for keeping the money that is a percentage of how much money you hold there.

And their policy is, "if you don't like it you are happy to withdraw your money and go somewhere else"

That assumes that you thrust your bank and government not to steal the saving. Hi form Argentina! Take a look at https://en.wikipedia.org/wiki/Corralito and the immediate follow-up.

Yes, that's the point. The money gets lent out for people to go out and do things they wouldn't otherwise be able to, causing economic activity. A simple example: If you needed a truck to perform a job, but you'd sit home doing nothing because you couldn't buy it outright, that'd be a loss to the economy. The risk of a default is priced into the interest rate.

Saving money in the form of hoarding is bad. If everyone does it, the economy slows down, we become materially poorer, because the amount of work we perform for each other is lowered. That's why there needs to be an incentive to invest money, through inflation and interest rates.

And the other side could argue that continuously investing in things puts you at continuous risk, and stops you from saving for a rainy day. Also, it's impossible even under deflation to hoard wealth completely, because you still need to buy food and clothes. Presumably, under deflation you would buy more necessities and consume less unnecessary things. Also, setting interest rates is a form of price control (on borrowing money), and maybe lenders should be allowed to respond to supply and demand organically like they can with every other good.

Without hard mathematics, these debates are pointless. I don't understand why you can't see that. This isn't physics.

(Disclaimer: I don't own crypto. I sold all of mine.)

There's no such thing as not putting yourself "at risk" when it comes to finance, or life in general. Even a hypothetical form of money that was perfectly stable puts you at risk of not benefiting from economic growth - the continuous refinement that happens unless we all just stop showing up for work.

Ultimately, this is a philosophical argument about human behavior that mathematics can't model, because our very beliefs shape the outcome. In other words: Dude trust me.

> Yes, that's the point. The money gets lent out for people to go out and do things

No not really, the bank does not need deposits for that, the bank can just create money and making an entry in a database and then just put that in the person loan account, that person then can use it for buying house/business etc.

Using savings then giving that savings as loans is an outdated concept.

If I earn a dollar I want its value to be as stable as possible for as long as possible. Why would anyone want to submit to top-down technocratic social engineering projects designed to change their behavior by manipulating the value of their money?

You're already participating in such a project. Every government currency is inflationary, their value trends towards zero over time. This is by design. Capitalists want you to spend that money as soon as possible instead of amassing vast amounts of it. They punish currency holders with inflation. If you don't spend the money or lend it out so others can spend it, the money loses part of its value. They want people spending and consuming constantly in order for the world to keep turning.

"Change their behavior" is quite the understatement.

All this causes is a massive amount of busywork just to have a shot at maintaining the value of your previous work. This is not necessary for a good economy, not to mention all the externalities it creates.

> Capitalists want you to spend that money as soon as possible instead of amassing vast amounts of it

No, capitalists want your money to be productive. You don't have to spend your money, though that is an option, you have many other options for what to do with your money.

> you have many other options for what to do with your money

That's what I meant by "or lend it out so others can spend it". That's what all those options come down to. Money cannot just sit in someone's accounts doing nothing, it must either be spent or given to someone else who will spend it: loans, investments.

The dollar has been amazingly stable over the last 50 years.

Outside of the last year, we haven’t broken the feds 2% inflation target for the majority of the last decade. Further, we haven’t experienced high inflation for the vast majority of of time that we’ve been off of the gold standard. Yet, the crypto maximalists run around like the US is Zimbabwe.

The dollars you made in the beginning of your career, 50 years ago, would be quite few relatively. Every year you can buy a little less for it. So you need to work twice for your money, once to acquire it and once more to keep its value by investing or w/e scheme you come up with. Stable, possibly. Good for the common man? Disagree.

he or she just said. with bitcoin, the value of your dollar is going up. that sounds great, but it creates a pressure to not spend and means that the relative value of your debts are also going up

I get that you don't want The Powers That Be to have any control over anything, including your money. but we live in a collaborative economy. if your neighbor doesn't spend it hurts you, and vice versa. monetary policy allows the system to work, whether most people understand it or not

Because when everyone else stops investing, and starts hoarding their dollars due to deflationary pressures, the economy stops, and so does your ability to earn dollars.

I don't like brushing my teeth, but it's preferable to getting meth-mouth.

Because that change in behavior is what lets markets work. With an inflationary currency, people want to create more wealth which is a net benefit to a society. With a deflationary currency, investing in the real world loses money, which disincentivizes projects that make the world better.

The problem with these purely verbal arguments is that they can be made to sound convincing either way.

E.g. Inflation is good because it encourages people to invest in things, creating jobs. However, inflation is bad because it encourages people to take unnecessary financial risks (like borrowing or lending money) when they could instead save it for a rainy day.

Saving the money for a rainy day is what strangles the economy. The economy's health is, to an approximation, the rate at which people spend money.

Slow the rate at which money flows through the economy, and bam, welcome to a recession/depression.

It's not a question of morality, as much as it's a question of mathematics. You may consider saving to be virtuous, and debt to be sinful, and sure, fine, that is your value system, but the only reason any of us have work is because we all spend, as opposed to save.

You can envision a society where people mostly work for themselves, where this wouldn't be an issue. Unfortunately, modern society relies on specialization, and I can't make most of the things I need by myself.

All those doom and gloom you describe only happens if Bitcoin is the only currency in the world. It doesn’t happen when Bitcoin is supplementary to USD, EUR, CNY, etc.

This is similar to how the proponents of free market and central plan both think the other side is pure evil. In the real world, a functioning economy is a mixture of both.

This is exactly like how I will go to my doctor when I feel sick. But I'll also drink my own urine to cure myself. It's important to have a little bit of a mix.

If you have a counterpoint then by all means make an argument for it, but don't post.. this.

It's always disappointing to see what hacker news devolves into whenever cryptocurrencies are discussed. We should try to hold ourselves to a higher standard than this.

Bitcoin can inflate. It's just that in order to change the current agreement on what Bitcoin is and how it works, you need a majority of mining power to agree, but the Bitcoin community has been famously conservative and unwilling to any kind of change. The reason? Probably a small amount of fear, and a huge investment in ASICs that would not be able to work if Bitcoin changes.

Also the Bitcoin community is, almost by definition, made up of people holding a lot of Bitcoin. They have a strong financial incentive to make sure that it deflates instead of inflates so that each Bitcoin becomes worth more over time instead of less.

This is why I take dogecoin more seriously than most coins out there. Most coins have some built in deflation as a scheme to make money, such as Bitcoin's limited number of coins or Ethereum's burn mechanism. If you want people to spend money, you can't have hoarding it be the most incentivized means of using it. Dogecoin has a ~3% long term inflation, which is pretty inline with real world currencies.

Disclaimer: I may be absolutely in the wrong here, as I may be missing some fundamental economics knowledge.

From my understanding, inflation is not really a property of the currency, but a property of market in which given currency is used. It's not the USD that loses value, it's the specific prices that increase, not that some products get cheaper. If some country suffered from hyper-inflation, they may start using USD instead of their original currency, and local products would end up with a different inflation in USD, than USD in US.

In Bitcoin and other crypto, I doubt there is huge market which has prices set in those cryptos - they are used as a courier money for markets in specific fiat currencies, like USD. I doubt people pay 0.001 BTC for a server, they pay $100 but in BTC.

It is a function of the total quantity of the currency at any given time, that currencies distribution across the economy, and the supply of the products/services it is being used for trade.

Then the banking system gets involved and it gets a bit complicated, but essentially any currency that is used for fractional reserve banking will experience a slow (or fast, depends on regulatory control) expansion in its total quantity over time.

Of course nobody would perform unregulated fractional reserve banking with cryptocurrencies now would they? Well actually, this is exactly what tether, luna etc are/were doing under the hood.

> A deflationary currency makes certain low margin economic activity extremely unattractive

There's absolutely nothing that prevents low margin activity from becoming high margin activity. You just need to raise the price. And if there's no consumer willing to pay the raised price, is that activity a really good idea?

> Inflation encourages spending

> Incentive to spend.

So less crap being produced and bought in a whim and more decision making process on purchasing long lasting quality products (like it used to be). Less cheap plastic trinkets, less planed obsolescence.

Please sign me up for that wonderful deflationary world!

> So less crap being produced and bought in a whim and more decision making process on purchasing long lasting quality products (like it used to be). Less cheap plastic trinkets, less planed obsolescence.

Not really. Just more cash held instead of productive assets. The only thing a deflationary currency chang's about an economy is giving everyone a default investment strategy that wastes output.

Saving in a period of high inflation doesn't work if your interest rate is lower than the inflation level. Irrespective of that, inflation definitely has an effect at the extreme ends. If the price of bread increases every hour, you'd better get in line at the shop first thing in the morning. If inflation is zero or negative, then you might consider skipping meals so you can save today's bread money, which will be worth more in the future.

The real effects of a deflationary currency are unknown. The side effects of a change of this nature are, likely, so vast that they are impossible to anticipate. That's the general problem with revolutions of this nature, they sound good on paper but it's mostly first level thinking. Ok, you got your change. What next? I see things like communism and anarchism the same way. It's laser focusing on a very small number of the ills of the current system without considering any of the good things that come with it and how to, at least, maintain them.

>Inflation at certain levels is good and necessary.

This is just flat-out misinformation! The US currency experienced deflation though much of the late 19th century yet GDP grew faster than nowadays, which clearly falsifies the notion that inflation is "necessary".

> Some of the worst economic crises in history, including the great depression, were marked by significant deflation.

But literally "the worst economic crisis in history" happened on the watch of an inflationary central bank.

Moreover, during the greatest worldwide deflationary period ever the united states went from literally a war ravaged country that had just decimated (lost 10%) of its population to "world power" in 50 years, while also enjoying decreasing economic inequality and increasing quality of life across the board not to mention managing to manumit a huge chunk of its population.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}